8 Vital Realities to Master HELOC vs Home Equity Loan Options in 2026

The financial world has a funny way of shifting just when you think you’ve got it figured out. If you’re sitting in your living room in April 2026, looking at the four walls around you and wondering how to fund that major renovation or consolidate high-interest debt, you aren’t alone. With the 30-year fixed-rate mortgage recently dipping to a more manageable 6.23%, many homeowners are feeling a renewed sense of financial agility.

However, the question remains: should you choose a HELOC vs home equity loan? , I can tell you that “intent” is everything. Choosing the wrong tool isn’t just a technical error—it’s a long-term financial anchor. In this guide, we’re stripping away the jargon to give you a natural, transparent look at how these products stack up in today’s 2026 market.

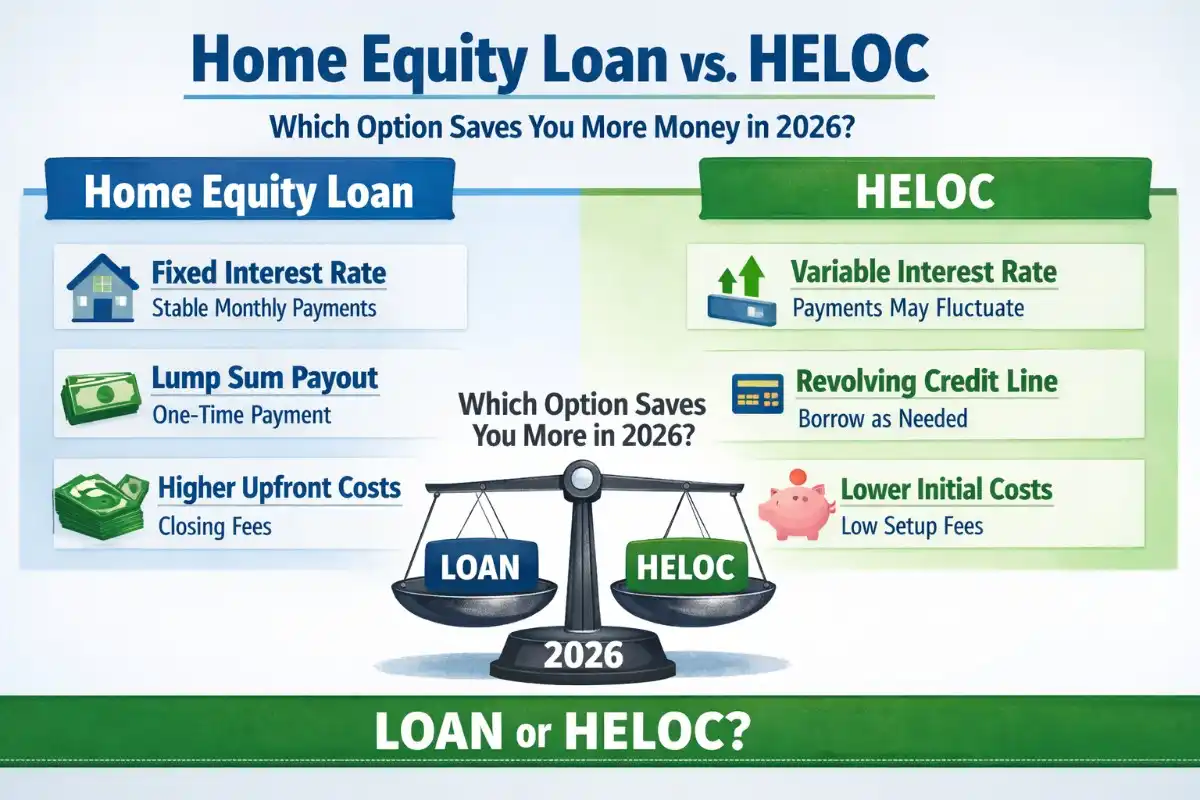

1. The Core Mechanical Difference

To understand the HELOC vs home equity loan debate, you first have to understand the shape of the debt.

- Home Equity Loan: This is a “second mortgage” that provides a lump sum of cash upfront. You pay it back at a fixed interest rate over a set term (usually 5 to 30 years).

- HELOC (Home Equity Line of Credit): This is a revolving line of credit, much like a credit card tied to your house. You draw what you need, pay it back, and draw again during the “draw period,” which typically lasts 10 years.

In 2026, the HELOC vs home equity loan choice often boils down to predictability versus flexibility. If you know exactly how much your kitchen remodel costs, the loan is your friend. If you’re paying for a wedding or college tuition over several years, the HELOC is the winner.

2. 2026 Rate Snapshot: What Will You Pay?

Interest rates have cooled since the highs of 2024, but they are still a major factor in the HELOC vs home equity loan comparison. Currently, HELOCs often start with a lower “introductory” rate, while home equity loans offer the security of a permanent fixed rate.

Estimated Rate Comparison (April 2026)

| Feature | HELOC vs Home Equity Loan | Interest Rate (Approx.) | Rate Type |

| Introductory HELOC | First 6 months | 4.90% – 5.25% | Tiered Fixed |

| Standard HELOC | Variable Period | 6.75% + Margin | Variable |

| Home Equity Loan | Fixed 15-Year | 7.50% – 9.00% | Fixed |

| Primary Mortgage | 30-Year Fixed | 6.23% | Reference Point |

As you can see, comparing a HELOC vs home equity loan requires looking past the first year. A variable rate can be dangerous if the Fed decides to tighten again later in 2026.

3. The 2026 Tax Update: It’s About the “Why”

Many homeowners search for HELOC vs home equity loan options specifically for tax relief. Under the current 2026 IRS rules (reinforced by the One Big Beautiful Bill Act), the interest on both products is deductible only if the funds are used to “buy, build, or substantially improve” the home securing the loan.

If you use a HELOC vs home equity loan to pay off a credit card or take a vacation, you lose that deduction. In a year where every tax dollar counts, the intended use of your funds should heavily influence your HELOC vs home equity loan decision.

4. Repayment Structures: The Hidden “Cliff”

One of the most dangerous aspects of the HELOC vs home equity loan comparison is the repayment phase.

- With a home equity loan, you start paying principal and interest immediately. It’s a straight line to zero debt.

- With a HELOC, many borrowers opt for “interest-only” payments during the 10-year draw period.

The “cliff” occurs when the draw period ends and you enter the repayment phase. In 2026, many homeowners who took out HELOCs in 2016 are finding their monthly payments doubling overnight. When deciding between a HELOC vs home equity loan, ask yourself if you have the discipline to handle a fluctuating payment.

5. Which is Better for Debt Consolidation?

As an SEO specialist, I see “debt consolidation” as the top secondary keyword for HELOC vs home equity loan searches. If you are drowning in 24% APR credit card debt, either option is a life raft. However, the fixed nature of a home equity loan is usually better here. It forces you into a structured payoff plan, whereas a HELOC might tempt you to spend back up to your limit once you’ve cleared your cards.

6. Closing Costs and Fees in 2026

Another pivotal point in the HELOC vs home equity loan battle is the cost of entry.

- HELOCs generally have lower (or zero) closing costs and fewer requirements for full appraisals.

- Home Equity Loans often mirror primary mortgages, requiring title insurance, appraisal fees, and origination charges that can total 2% to 5% of the loan amount.

If you only need $20,000, the high closing costs of a home equity loan might negate the benefits, making the HELOC vs home equity loan choice lean toward the credit line.

7. The SEO Perspective: Experience Matters

In 2026, search engines prioritize E-E-A-T (Experience, Expertise, Authoritativeness, and Trustworthiness). When you read about HELOC vs home equity loan online, look for personal anecdotes. Real financial advice acknowledges that your home is your sanctuary, not just a line on a spreadsheet. Any path you choose in the HELOC vs home equity loan debate involves using your home as collateral. If you can’t pay, the bank can take the house.

8. Strategies for the 2026 Borrower

To win the HELOC vs home equity loan game this year, follow this checklist:

- Calculate Your Equity: Most lenders require you to keep 15-20% equity in the home.

- Audit Your Project: If it’s a one-time cost, choose the loan. If it’s ongoing, choose the HELOC.

- Check Your Score: A 740+ credit score is the “golden ticket” for both products in 2026.

- Consider a Hybrid: Some 2026 lenders offer a “fixed-rate HELOC,” giving you the flexibility of a line with the security of a fixed rate on the portion you’ve already spent.

Frequently Asked Questions (FAQs)

Which is easier to qualify for: HELOC vs home equity loan?

Generally, they have similar requirements. However, some fintech lenders in 2026 offer faster, AI-driven approvals for HELOCs with fewer document requirements than a traditional home equity loan.

Can I have both a HELOC and a home equity loan?

Yes, but you must have enough equity to cover both, plus your primary mortgage. Most lenders limit your total combined loan-to-value (CLTV) to 85%.

Does a HELOC vs home equity loan affect my credit score differently?

A home equity loan is seen as an “installment loan,” while a HELOC is “revolving credit.” Maxing out a HELOC can lower your score by increasing your credit utilization, even if you never miss a payment.

What happens if home prices drop in late 2026?

If you have a home equity loan, your payment stays the same. If you have a HELOC, the lender can actually “freeze” or reduce your credit line if they believe your home’s value has fallen below a certain threshold.

Are closing costs deductible for a HELOC vs home equity loan?

Generally, no. Closing costs are not deductible in the year you pay them, but they may be added to the cost basis of your home, which could help reduce capital gains taxes when you eventually sell.

Final Thoughts for 2026 Homeowners

The choice between a HELOC vs home equity loan isn’t about which product is “better”—it’s about which one fits your life. In April 2026, with the economy showing signs of cautious optimism, your home’s equity is a powerful financial tool.

If you crave the peace of mind that comes with a “set it and forget it” monthly bill, the home equity loan is your champion. If you want a safety net that only costs you money when you actually use it, the HELOC is the way to go. Regardless of which side of the HELOC vs home equity loan fence you land on, remember that your home is the foundation of your wealth. Treat it with respect, shop for the best APR, and always ensure your borrowing supports your long-term goals. Your future self will thank you for making an informed HELOC vs home equity loan choice today.